Insurance Expansion and Social Protection in India

1. India ranked as the 10th largest insurance market globally in 2024–25 by nominal premium volume, with a global market share of 1.8 percent.

2. Insurance penetration in India stood at 3.7 percent in 2024–25, with life insurance at 2.7 percent and non-life insurance at 1 percent.

3. Insurance density in India increased to USD 97.0 in 2024–25, indicating a marginal rise in per capita premium spending.

4. During FY 2024–25, the insurance sector issued 41.84 crore policies, collected premiums worth ₹11.93 lakh crore, and paid claims amounting to ₹8.36 lakh crore.

5. Assets under management in the insurance sector stood at ₹74.44 lakh crore as on 31 March 2025, showing the expanding scale of long-term financial intermediation.

6. The share of insurance and pension funds in household financial assets rose from 28.6 percent in FY 2018–19 to 29.6 percent in FY 2024–25.

7. Total premium income grew from ₹8.30 lakh crore in FY 2020–21 to ₹11.90 lakh crore in FY 2024–25, recording growth of 43.37 percent.

8. Life insurance premiums increased from ₹6.30 lakh crore in FY 2020–21 to ₹8.86 lakh crore in FY 2024–25, while non-life premiums rose from ₹2.02 lakh crore to ₹3.10 lakh crore.

9. Life insurance accounted for 91 percent of total assets under management and around 74 percent of total premium income, remaining the dominant segment of the sector.

10. Within non-life insurance, health insurance emerged as the leading business line, contributing 41 percent of gross domestic premium and surpassing motor insurance.

11. The number of insurers’ offices increased from 21,338 in March 2024 to 22,076 in March 2025, while the distribution network expanded from about 48 lakh in FY 2020–21 to nearly 83 lakh in FY 2024–25.

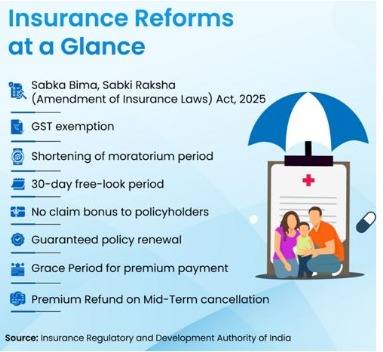

12. Under the Sabka Bima, Sabki Raksha Act, 2025, the FDI limit in Indian insurance companies was raised from 74 percent to 100 percent.

13. GST exemption on all individual life insurance policies, health insurance policies including family floaters, and reinsurance came into effect from 22 September 2025.

14. PMJJBY, launched in May 2015, provides life cover of ₹2 lakh at an annual premium of ₹436 and recorded 26.88 crore enrolments with 10,45,450 claims disbursed by February 2026.

15. PMFBY, launched in February 2016, received 93.98 crore applications and paid claims worth ₹1,94,505.9 crore by 13 March 2026, while farmers pay maximum premiums of 2 percent, 1.5 percent, and 5 percent for notified crop categories.

Must Know Terms :

1.PMJJBY

PMJJBY (Pradhan Mantri Jeevan Jyoti Bima Yojana) is a one-year renewable term life insurance scheme launched in May 2015. It provides life cover of ₹2 lakh to bank account holders aged 18 to 50 years at an annual premium of ₹436. The premium is auto-debited. By February 2026, the scheme recorded 26.88 crore enrolments and 10,45,450 claims disbursed nationwide overall.

2. PMSBY

PMSBY (Pradhan Mantri Suraksha Bima Yojana) is an accidental insurance scheme launched in May 2015 for savings bank account holders aged 18 to 70 years. At an annual premium of ₹20, it provides ₹2 lakh cover for accidental death or full disability and ₹1 lakh for partial disability. By February 2026, 57.11 crore enrolments and 1.76 lakh claims were recorded.

3. PMFBY

PMFBY (Pradhan Mantri Fasal Bima Yojana) was launched in February 2016 to provide affordable and comprehensive crop insurance against non-preventable natural risks. Farmers pay maximum premiums of 2 percent for Kharif food and oilseed crops, 1.5 percent for Rabi crops, and 5 percent for annual commercial or horticultural crops. By 13 March 2026, 93.98 crore applications were received under it.

4. ABPMJAY

AB-PMJAY (Ayushman Bharat Pradhan Mantri Jan Arogya Yojana) was launched in September 2018 and provides free health insurance cover of up to ₹5 lakh per family per year for secondary and tertiary care. It covers pre-existing diseases from day one and allows nationwide portability. In September 2024, coverage was expanded to citizens aged 70 years and above, irrespective of income.

5. IRDAI

IRDAI (Insurance Regulatory and Development Authority of India) is the insurance sector regulator that leads the vision of Insurance for All by 2047. It introduced key reforms such as reducing the health insurance moratorium period from 8 years to 60 months, standardising a 30-day free-look period, guaranteeing policy renewal except in fraud cases, and strengthening portability, consumer choice, and protection.

6. ESI

ESI (Employees’ State Insurance) is a social security scheme that protects employees against sickness, maternity, disablement, and death due to employment injury, while also providing medical care to insured persons and their families. As on 31 March 2025, it covered 3.24 crore employees and 3.84 crore insured persons, including 83.1 lakh insured women, with 14.91 crore beneficiaries under the scheme.

Key Takeways

a) India ranks as the 10th largest insurance market globallyby premium volume (Swiss Re Report).

b) Share of insurance and pension funds in household financial assetsrose to 6% in FY25 from 28.6% in FY19, as per Economic Survey 2025-26.

c) FDI limit in insurance raised to 100%under the Sabka Bima, Sabki Raksha (Amendment of Insurance Laws) Act, 2025.

d) Pradhan Mantri Jeevan Jyoti Bima Yojana recorded 26.88 crore enrolmentsand 45 lakh claims disbursed (as of Feb 2026).

MCQ :

1. With reference to India’s insurance sector in 2024–25, consider the following statements:

1. India ranked as the 10th largest insurance market globally by nominal premium volume.

2. Its global market share stood at 1.8 percent.

3. Insurance density stood at USD 97.0.

Which of the statements given above are correct?

A) 1 and 2 only

B) 2 and 3 only

C) 1 and 3 only

D) 1, 2 and 3

2. Insurance penetration in India during 2024–25 stood at:

A) 2.7 percent

B) 3.7 percent

C) 4.7 percent

D) 1.8 percent

3. During FY 2024–25, the insurance sector collected premium income of:

A) ₹8.36 lakh crore

B) ₹11.93 lakh crore

C) ₹74.44 lakh crore

D) ₹8.86 lakh crore

4. As on 31 March 2025, assets under management in the insurance sector stood at:

A) ₹41.84 lakh crore

B) ₹11.93 lakh crore

C) ₹74.44 lakh crore

D) ₹8.30 lakh crore

5. The share of insurance and pension funds in household financial assets increased from 28.6 percent in FY 2018–19 to what level in FY 2024–25?

A) 29.6 percent

B) 30.6 percent

C) 27.6 percent

D) 31.6 percent

6. Consider the following statements regarding premium growth between FY 2020–21 and FY 2024–25:

1. Total premium income grew by 43.37 percent.

2. Life insurance premiums grew by 40.63 percent.

3. Non-life insurance premiums grew by 53.46 percent.

Which of the statements given above are correct?

A) 1 and 2 only

B) 2 and 3 only

C) 1 and 3 only

D) 1, 2 and 3

7. Which one of the following correctly describes the dominant segment of India’s insurance sector?

A) Non-life insurance accounts for 91 percent of total assets under management

B) Life insurance accounts for 91 percent of total assets under management

C) Health insurance accounts for 74 percent of total premium income

D) Motor insurance is the leading non-life business line

8. Within the non-life insurance segment, the leading business line in India is:

A) Marine insurance

B) Motor insurance

C) Health insurance

D) Crop insurance

9. The Sabka Bima, Sabki Raksha Act, 2025 raised the FDI limit in Indian insurance companies from:

A) 49 percent to 74 percent

B) 51 percent to 100 percent

C) 74 percent to 100 percent

D) 26 percent to 74 percent

10. GST exemption on individual life insurance policies, health insurance policies including family floater, and reinsurance came into effect from:

A) 22 September 2025

B) 30 December 2025

C) 23 April 2026

D) 31 March 2025

11. PMJJBY provides life cover of:

A) ₹1 lakh

B) ₹5 lakh

C) ₹3 lakh

D) ₹2 lakh

12. With reference to PMJJBY, consider the following statements:

1. It was launched in May 2015.

2. It provides life cover of ₹2 lakh.

3. The annual premium is ₹436.

Which of the statements given above are correct?

A) 1 and 2 only

B) 2 and 3 only

C) 1 and 3 only

D) 1, 2 and 3

13. PMSBY provides an annual accidental insurance cover of ₹2 lakh in case of:

A) Partial disability only

B) Accidental death or full disability

C) Any hospitalisation

D) Natural death

14. Under PMFBY, farmers pay a maximum premium of 1.5 percent for:

A) Annual commercial crops

B) Kharif food and oilseed crops

C) Rabi food and oilseed crops

D) Horticultural crops

15. As on 31 March 2025, the Employees’ State Insurance Scheme covered:

A) 3.24 crore employees and 3.84 crore insured persons

B) 3.84 crore employees and 3.24 crore insured persons

C) 14.91 crore employees and 83.1 lakh insured women

D) 26.88 crore employees and 10.45 lakh claims

0 comment