India Digital Payment Transformation

1. Unified Payments Interface (UPI) became the core of India’s fast payment ecosystem, transforming person-to-person and merchant transactions since 2016 through instant transfers, interoperability, low cost access, and widespread usability.

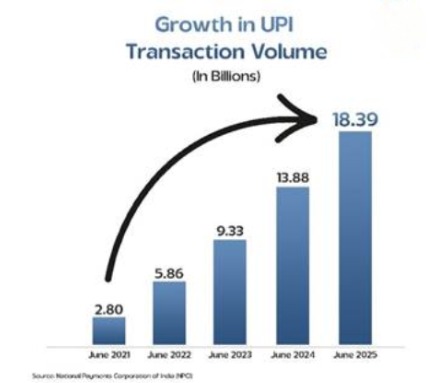

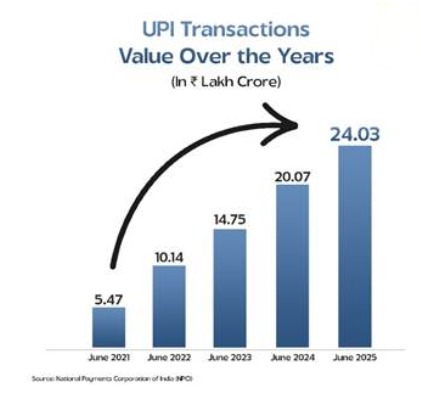

2. In June 2025, UPI processed 18.39 billion transactions worth ₹24.03 lakh crore, showing massive scale and reflecting about 32 percent annual growth over June 2024 levels.

3. The platform serves 491 million individuals and 65 million merchants, while linking 675 banks into one unified network that enables seamless fund transfers across apps.

4. UPI now accounts for 85 percent of all digital transactions in India, showing its dominance over alternative payment modes and confirming its central place.

5. The International Monetary Fund (IMF) noted that India contributes nearly 50 percent of global real-time digital payments, making UPI a major international benchmark.

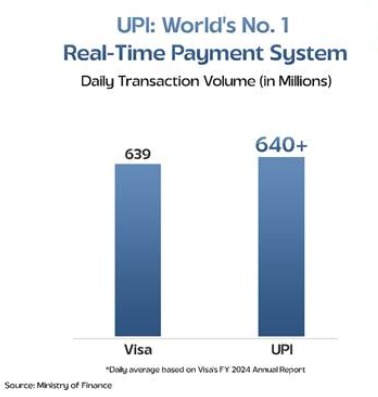

6. UPI processes more than 640 million transactions daily, slightly surpassing Visa’s 639 million, establishing itself as the world’s leading real-time payment system within nine years.

7. The system is already operational in seven countries, including the UAE (United Arab Emirates), Singapore, Bhutan, Nepal, Sri Lanka, France, and Mauritius.

8. France became UPI’s first entry point into Europe, marking a significant milestone in international expansion and enabling smoother digital payments for Indians travelling or residing there.

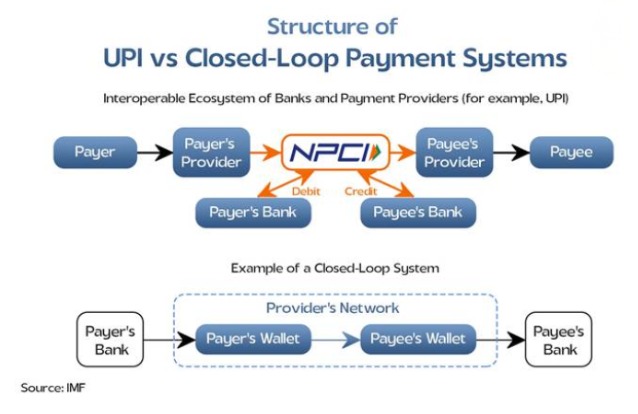

9. UPI’s success rests heavily on interoperability, allowing users from different banks and apps to transact freely under common technical, legal, and operational standards.

10. Before UPI, digital payments were fragmented through closed-loop systems, where transactions stayed within one wallet or provider, limiting convenience, competition, and broader payment network efficiency.

11. By connecting banks and fintech applications on one common platform, UPI gave users freedom to choose any app while encouraging better features, stronger security, and service innovation.

12. UPI has normalized instant, round-the-clock transactions for bill payments, shopping, donations, mobile recharges, merchant purchases, and Quick Response (QR) code based payments in everyday life.

13. Pradhan Mantri Jan Dhan Yojana created the financial base for UPI’s growth, with more than 55.83 crore bank accounts opened by 9 July 2025 nationwide.

14. Aadhaar strengthened the digital backbone by providing secure biometric identity, with over 142 crore cards generated cumulatively by 30 June 2025 across India.

15. Affordable connectivity accelerated adoption, supported by 4.74 lakh active Fifth Generation (5G) base stations, 116 crore mobile subscribers, and sharply reduced internet data costs nationwide.

Must Know Terms :

1. Interoperability

Interoperability is the feature that allows different banks and payment apps to work together on one payment network. In UPI, it lets a user send money from one app to another regardless of bank or platform. This common structure helped remove closed payment silos, widened user choice, increased competition among providers, and accelerated daily digital payment adoption across India nationwide.

2.Authentication

Authentication is the process of verifying that the correct user is making a transaction. In the UPI system, payments are secured through two-step authentication, making transfers fast while maintaining safety. This mechanism reduces fraud risk and supports trust in digital payments. Reliable authentication has been one of the important reasons UPI became widely accepted by individuals, merchants, and service providers nationally.

3.Biometrics

Biometrics refers to physical identity markers such as fingerprints or iris data used for verification. Aadhaar is built on biometric identification and has provided India with a large digital identity base. This identity infrastructure helped strengthen authentication and service delivery across digital systems. By 30 June 2025, over 142 crore Aadhaar cards had been generated cumulatively, supporting broad access to formal digital services.

4.Fintech

Fintech means technology-based financial service providers that use digital platforms to offer payment, lending, and related services. In the UPI ecosystem, fintech apps connect with banks through a common platform, allowing people to transact using different applications. Their participation increased convenience, app choice, feature innovation, and service competition. This partnership between banks and fintech firms helped UPI become part of everyday payments.

5.Remittances

Remittances are money transfers sent by individuals from one place to another, often across regions or countries. The expansion of UPI beyond India is expected to improve remittance efficiency by making transfers faster, smoother, and more accessible. India is also pushing for wider adoption of UPI standards within BRICS, which could strengthen cross-border financial flows, inclusion, and digital payment connectivity among member countries.

6.Redressal

Redressal means the process of resolving complaints, disputes, or transaction-related problems. In the UPI ecosystem, users can report payment issues directly through the app, making grievance handling easier and more accessible. This built-in complaint support improves user confidence in digital payments. Easy redressal is important because a payment system used daily by millions must also provide quick problem resolution mechanisms.

Key Takeaways

a. IMF notes that India is the global leader in fast payments.

b. ₹24 lakh crore processed via 18.39 billion UPI transactions in June 2025.

c. UPI powers 85% of India’s digital payments and nearly 50% globally.

d. UPI handles 640+ million transactions daily, ahead of Visa.

MCQ :

1. Unified Payments Interface was launched in:

A) 2014

B) 2015

C) 2016

D) 2017

2. In June 2025, UPI processed transactions worth:

A) ₹18.39 lakh crore

B) ₹24.03 lakh crore

C) ₹13.88 lakh crore

D) ₹32.00 lakh crore

3. The number of UPI transactions recorded in June 2025 was:

A) 16.39 billion

B) 17.39 billion

C) 18.39 billion

D) 19.39 billion

4. The annual growth in UPI transactions over June 2024 was about:

A) 22 percent

B) 27 percent

C) 32 percent

D) 37 percent

5. The UPI platform serves how many individuals?

A) 491 million

B) 675 million

C) 65 million

D) 142 million

6. The number of merchants connected with UPI is:

A) 55 million

B) 75 million

C) 65 million

D) 85 million

7. UPI links how many banks on one platform?

A) 575

B) 625

C) 675

D) 725

8. UPI now accounts for what share of all digital transactions in India?

A) 75 percent

B) 80 percent

C) 85 percent

D) 90 percent

9. India contributes nearly what share of global real-time digital payments?

A) 30 percent

B) 40 percent

C) 50 percent

D) 60 percent

10. UPI processes more than how many transactions daily?

A) 540 million

B) 590 million

C) 620 million

D) 640 million

11. Which country marked UPI’s first entry into Europe?

A) Singapore

B) France

C) Mauritius

D) Nepal

12. UPI is already operational in how many countries?

A) Five

B) Six

C) Seven

D) Eight

13. Before UPI, digital payments were largely limited by:

A) Open network systems

B) Closed-loop systems

C) Blockchain clearing houses

D) Central bank wallets

14. More than how many Jan Dhan accounts had been opened by 9 July 2025?

A) 45.83 crore

B) 50.83 crore

C) 55.83 crore

D) 60.83 crore

15. By 30 June 2025, over how many Aadhaar cards had been generated cumulatively?

A) 132 crore

B) 137 crore

C) 140 crore

D) 142 crore

0 comment