Financial Inclusion Progress in India

“Economic growth cannot only be restricted to a few cities and a few citizens. Development has to be all-round and all-inclusive.”

– PM Narendra Modi

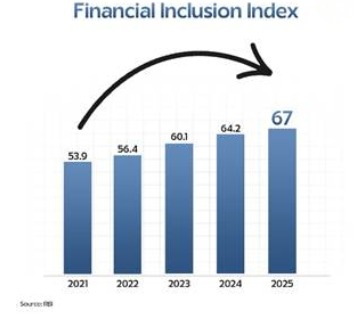

1. Reserve Bank of India’s Financial Inclusion Index reached 67.0 for the year ending March 2025, rising from 64.2 in March 2024 and showing broad improvement nationwide.

2. Since its launch in 2021, the Financial Inclusion Index has increased by 24.3 percent, reflecting stronger access, usage, service quality, and expanding financial literacy initiatives across India.

3. The Financial Inclusion Index is built on 97 indicators and uses a 0 to 100 scale, where 0 means no inclusion and 100 complete inclusion.

4. The index has three sub-indices: Access, Usage, and Quality, carrying respective weights of 35 percent, 45 percent, and 20 percent in the overall financial inclusion assessment.

5. Access measures supply-side availability of financial services through 26 indicators covering banking, digital systems, pension, and insurance, along with supporting infrastructure such as accounts, offices, and terminals.

6. Usage represents demand-side financial participation through 52 indicators, tracking savings, investments, insurance, credit, direct benefit transfers, and the volume and value of UPI transactions.

7. Quality is measured through 19 indicators covering financial literacy, consumer protection, inequality, safe usage practices, and grievance redressal mechanisms within the broader financial services framework.

8. Global Findex 2025 recorded India’s account ownership at 89 percent, indicating major progress since 2011 in expanding formal financial participation and increasing the share of adults.

9. National Strategy for Financial Inclusion 2019–2024 aimed to ensure every village had access to a formal financial service provider within a five-kilometre radius.

10. National Strategy for Financial Education 2020–2025 adopted a 5-C approach built around Content, Capacity, Community-led communication, Communication strategy, and Collaboration among multiple stakeholders nationwide.

11. Pradhan Mantri Jan Dhan Yojana had over 55.98 crore beneficiaries by 4 August 2025, with women holding more than 55 percent accounts nationwide.

12. A network of 13.55 lakh Bank Mitras was created for last-mile banking outreach, while 107 Digital Banking Units were operational by December 2024.

13. Pradhan Mantri Suraksha Bima Yojana reached cumulative enrolment of 50.54 crore individuals by 19 March 2025, offering accidental death and disability cover for ₹20 annually.

14. Atal Pension Yojana crossed 7.65 crore subscribers by April 2025, with a corpus of ₹45,974.67 crore and women constituting about 48 percent subscribers.

15. Kisan Credit Card operative accounts rose from ₹4.26 lakh crore in March 2014 to ₹10.05 lakh crore in December 2024, benefiting 7.72 crore farmers.

Must Know Terms :

1. Bankmitra

Bankmitra is a banking correspondent used for last-mile delivery of formal financial services in underserved areas. This model helps people open accounts, withdraw cash, deposit money, and access direct benefit-linked banking facilities. The outreach structure included 13.55 lakh Bank Mitras. It worked alongside 107 Digital Banking Units operational by December 2024, strengthening physical and assisted access beyond conventional branch networks.

2.Redressal

Redressal is the institutional process for resolving customer complaints, transaction disputes, and service deficiencies in formal finance. It is treated as a measurable quality factor in the Financial Inclusion Index, not a peripheral issue. Strong redressal improves consumer trust, especially for first-time users of banking, pensions, insurance, and digital payments. Its inclusion within the Quality segment shows that usable finance must also be accountable.

3.Operative

Operative means active in practice, not merely opened or sanctioned on paper. In credit systems, operative accounts indicate real and continuing usage by beneficiaries. Kisan Credit Card operative accounts rose from ₹4.26 lakh crore in March 2014 to ₹10.05 lakh crore in December 2024. This reflected expansion in effective agricultural credit access and showed that formal inclusion was translating into functioning, transaction-based rural financial participation.

4.Corpus

Corpus means the total accumulated fund available within a scheme after sustained contributions over time. It indicates both scale and financial depth. Atal Pension Yojana recorded a corpus of ₹45,974.67 crore by April 2025. The scheme also crossed 7.65 crore subscribers, with women forming about 48 percent. This made corpus size an important indicator of pension penetration, long-term savings mobilisation, and social security expansion.

5.Enrolment

Enrolment refers to the cumulative number of registered participants under a particular scheme. It is a direct measure of outreach and public acceptance. Pradhan Mantri Suraksha Bima Yojana recorded cumulative enrolment of 50.54 crore individuals by 19 March 2025. The scheme provided accidental death and disability cover at an annual premium of ₹20, making low-cost risk protection accessible to a very large population segment.

6.Subindices

Subindices are weighted component measures used to build a broader composite index. In the Financial Inclusion Index, the three subindices are Access, Usage, and Quality. Their respective weights are 35 percent, 45 percent, and 20 percent. The full index is based on 97 indicators and measured on a 0–100 scale. This structure captures service availability, actual participation, and effectiveness of financial delivery together.

Key Takeawys :

a) Financial Inclusion Index risen to 67 in 2025, up by 24.3% since 2021

- b) 55.98 crore beneficiaries under the revolutionaryPradhan Mantri Jan Dhan Yojana

- c) 6.65 Lakhs accounts opened in 1-month campaign for Saturation of Financial Inclusion Schemes

MCQ :

1. The Financial Inclusion Index for the year ending March 2025 stood at:

A) 64.2

B) 65.8

C) 66.4

D) 67.0

2. The Financial Inclusion Index had increased by what percentage since its launch in 2021?

A) 24.3 percent

B) 22.3 percent

C) 26.3 percent

D) 28.3 percent

3. The Financial Inclusion Index is constructed using how many indicators?

A) 87

B) 97

C) 107

D) 117

4. In the Financial Inclusion Index, the weight assigned to Usage is:

A) 35 percent

B) 20 percent

C) 45 percent

D) 25 percent

5. The number of indicators used to measure Access in the index is:

A) 26

B) 19

C) 52

D) 35

6. Which component of the Financial Inclusion Index is measured through 52 indicators?

A) Quality

B) Usage

C) Access

D) Infrastructure

7. The Quality segment of the Financial Inclusion Index is based on:

A) 15 indicators

B) 17 indicators

C) 19 indicators

D) 21 indicators

8. India’s account ownership recorded in Global Findex 2025 was:

A) 79 percent

B) 84 percent

C) 89 percent

D) 94 percent

9. National Strategy for Financial Inclusion 2019–2024 aimed to ensure formal financial service access within what distance of every village?

A) Three-kilometre radius

B) Five-kilometre radius

C) Seven-kilometre radius

D) Ten-kilometre radius

10. The National Strategy for Financial Education 2020–2025 adopted which approach?

A) 3-C approach

B) 4-C approach

C) 5-C approach

D) 6-C approach

11. Pradhan Mantri Jan Dhan Yojana had over how many beneficiaries by 4 August 2025?

A) 45.98 crore

B) 50.98 crore

C) 55.98 crore

D) 60.98 crore

12. The number of Bank Mitras created for last-mile banking outreach was:

A) 11.55 lakh

B) 12.55 lakh

C) 13.55 lakh

D) 14.55 lakh

13. Pradhan Mantri Suraksha Bima Yojana reached cumulative enrolment of:

A) 40.54 crore

B) 45.54 crore

C) 50.54 crore

D) 55.54 crore

14. Atal Pension Yojana crossed how many subscribers by April 2025?

A) 6.65 crore

B) 7.65 crore

C) 8.65 crore

D) 9.65 crore

15. Kisan Credit Card operative accounts rose to what level in December 2024?

A) ₹8.05 lakh crore

B) ₹9.05 lakh crore

C) ₹10.05 lakh crore

D) ₹11.05 lakh crore

0 comment